Introduction

Section 80CCC provides tax deductions on buying a new policy or continuing a policy that pays a pension.

Applicable for taxpayers who have deposited some amount out of their taxable income to buy or continue an annuity plan from LIC or any other insurer.

80CCC section of Income Tax Act

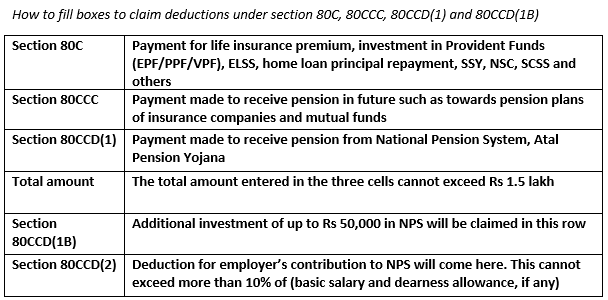

According to the Income Tax Department, individual taxpayers can claim tax deduction for “contributions to certain pension funds of LIC or any other insurer (up to Rs. 1,50,000) (subject to certain conditions)”. It further adds that “the aggregate amount of deductions under Section 80C, Section 80CCC and Section 80CCD shall not, in any case, exceed Rs. 1,50,000”.

Eligibility

Any individual taxpayer who has invested in an annuity plan offered by an insurer can claim the deductions under this section. Hindu Unified Families (HUF) cannot claim the benefits of this section. Also, both resident and non-resident individuals can claim the deductions u/s Section 80CCC.

Can I claim deductions under both Sections 80C and 80CCC?

The deductions u/s 80CCC are a part of the overall deductions’ u/s 80C. Deductions claimed under 80CCC is limited to Rs.1 lakh per year, while the deductions under 80C is limited to Rs.1.5 lakhs per year. 80CCC is a subset of 80C and so the overall deductions cannot exceed Rs.1.5 lakhs.

Pension Fund

A pension fund is an investment product which provides retirement income. Section 80CCC of the Income Tax Act, 1961 allows taxpayers to claim deductions for contributions made to certain pension funds. To claim this tax benefit, the individual has to make payments to receive pension from a fund, which is referred to under Section 10 (23AAB). The maximum deduction that the individual can claim under Section 80CCC is Rs. 1,50,000.

According to the Income Tax Department, Section 10(23AAB) reads “Any income of a fund set-up by the Life Insurance Corporation of India on or after August 1, 1996 or any other insurer to which contribution is made by any person for receiving pension from such fund, and which is approved by the Controller of Insurance or the Insurance Regulatory and Development Authority of India, is exempt from tax.”

Claim 80CCC deduction

For claiming the income tax benefit under section 80CCC you must

- Be an individual As per the provisions of section 80CCC to claim a deduction one must be an individual. It means the non-resident individuals (NRI) can also benefit from this section.

- Have a taxable income You can claim the tax benefit only when you have taxable income which can be adjusted against this deduction. If your income is below the basic exemption limit then there is no need for claiming the deduction.

- Make a contribution to specified pension funds The tax benefit can be availed only if you invest the money in specified funds during the relevant financial year.

- Make a contribution out of taxable income This is one of the most important points to be considered while claiming deduction under section 80CCC. The investment must be done out of your taxable income and should not be done from any other source.

Terms and Conditions of the 80CCC Section

Here is a list of terms and conditions for the 80ccc section:

- This 80CCC section is available to those individuals who have paid the sum for insurance renewal or purchase of a life insurance policy from their taxable income.

- In the terms of the Section 10 ( 23AAB) the payment of funds from the policy should be made from the accumulated funds.

- If any bonuses that are received or interest is accumulated, it is not eligible for deduction under Section 80CCC.

- Any amount received from the policy as a monthly pension is liable for taxation as per the prevailing rates.

- If the policy is surrendered, the amount would also be subject to taxation.

- Any rebates that were available on investment in annuity plans before April 2006 are not allowed under Section 88.

- Any amount that is deposited before April 2006 is not eligible for deduction.

Tax benefit allowed on investments u/s 80CCC

The following are the tax implications and benefits u/s 80CCC

- Investment Amount: You get a complete deduction upto Rs 1.5 lakh.

- Pension or Withdrawal amount received: This amount is fully taxable in the hands of the receiver.

- Interest or Bonus Received: The amount received shall also be fully taxable in the hands of the receiver.

Also, no tax benefit under section 80CCC will be allowed if you have already taken the benefit for this deduction under section 80C. The aggregate deduction under section 80C, 80CCC and 80CCD(1) cannot exceed Rs.1,50,000.