Introduction

Corporate Finance is the process of dealing with the company’s finances, capital structure, and management to increase the value of the company. Corporate finance also includes the tools and analysis utilized to prioritize and distribute financial resources.

The ultimate purpose of corporate finance is to maximize the value of a business through the planning and implementation of resources while balancing risk and profitability.

A company’s capital structure is crucial to maximizing the value of the business. Its structure can be a combination of long-term and short-term debt and/or common and preferred equity. The ratio between a firm’s liability and its equity is often the basis for determining how well balanced or risky the company’s capital financing is.

A company that is heavily funded by debt is considered to have a more aggressive capital structure and, therefore, potentially holds more risk for stakeholders. However, taking this risk is often the primary reason for a company’s growth and success.

Choosing between investment projects will thus be based upon several inter-related criteria.

(1) Corporate management seeks to maximize the value of the firm by investing in projects which yield a positive net present value when valued using an appropriate discount rate in consideration of risk.

(2) These projects must also be financed appropriately.

(3) If no growth is possible by the company and excess cash surplus is not needed to the firm, then financial theory suggests that management should return some or all of the excess cash to shareholders.

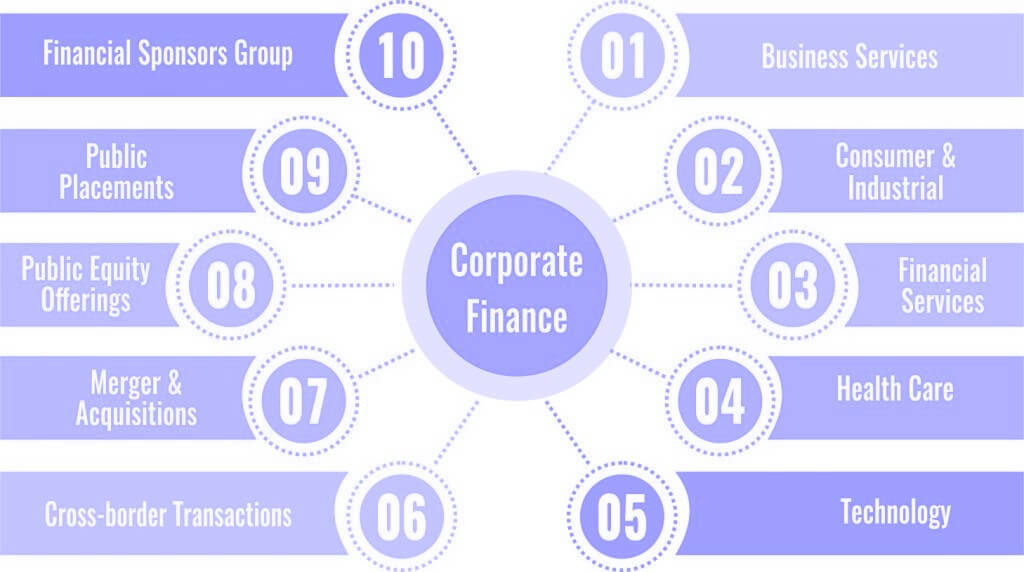

Parts of Corporate Finance

Capital Investments

Corporate finance tasks include making capital investments and deploying a company’s long-term capital. The capital investment decision process is primarily concerned with capital budgeting. Through capital budgeting, a company identifies capital expenditures, estimates future cash flows from proposed capital projects, compares planned investments with potential proceeds, and decides which projects to include in its capital budget.

Capital investment can come from various sources, such as financial institutions, angel investors, and venture capitalists, among others. Generally, startups and new companies are the ones who seek capital investments.

However, after having received investments, the invested amount must be utilized to develop and push the business ahead. In the same line, if a company announces to go public, the large amount of funds pooled in from the investors is also considered as a form of capital investment.

Capital Financing

Corporate finance is also responsible for sourcing capital in the form of debt or equity. A company may borrow from commercial banks and other financial intermediaries or may issue debt securities in the capital markets through investment banks. A company may also choose to sell stocks to equity investors, especially when it needs large amounts of capital for business expansions.

Financial capital comes primarily from equity and debt when you start your business. Over time, revenues give you more capital to work with.

Financial capital keeps your business running. It makes it possible for you to buy goods and services such as office equipment, factory equipment, vehicles, web design services and liability insurance. If you have employees, you pay their wages with capital.

After you start earning a profit, some of your capital comes from your revenues. When you start your business, you’ll probably need an outside source. Even established businesses often need additional capital financing.

Short-Term Liquidity

Short-term liquidity of an enterprise is measured by the degree to which it can meet its short-term obligation. Liquidity implies the ready ability to convert assets into cash or obtain cash.

The importance of short-term liquidity discuss given below:

- Liquidity is a matter of degree.

- Lack of liquidity prevents a company from taking advantage Of favorable discounts.

- It also implies limited opportunities and constraints on management actions.

- A company’s ability to cover current obligations.

- Short-term lead to the forced sale of investments and assets.

Short-term financial management may also involve getting additional credit lines or issuing commercial papers as liquidity backups.

Sources of capital

Debt Capital

Corporations may rely on borrowed funds (debt capital) as sources of investment to sustain ongoing business operations or to fund future growth. Debt comes in several forms, such as through bank loans, notes payable, or bonds issued to the public. Bonds require the corporations to make regular interest payments (interest expenses) on the borrowed capital until the debt reaches its maturity date, therein the firm must pay back the obligation in full.

Debt payments can also be made in the form of sinking fund provisions, whereby the corporation pays annual installments of the borrowed debt above regular interest charges. Corporations that issue callable bonds are entitled to pay back the obligation in full whenever the company feels it is in their best interest to pay off the debt payments.

If interest expenses cannot be made by the corporation through cash payments, the firm may also use collateral assets as a form of repaying their debt obligations (or through the process of liquidation).

Equity Capital

Corporations can alternatively sell shares of the company to investors to raise capital. Investors, or shareholders, expect that there will be an upward trend in value of the company (or appreciate in value) over time to make their investment a profitable purchase.

Shareholder value is increased when corporations invest equity capital and other funds into projects (or investments) that earn a positive rate of return for the owners. Investors prefer to buy shares of stock in companies that will consistently earn a positive rate of return on capital in the future, thus increasing the market value of the stock of that corporation.

Preferred Stock

Preferred stock is an equity security which may have any combination of features not possessed by common stock including properties of both an equity and a debt instrument, and is generally considered a hybrid instrument. Preferred are senior (i.e. higher ranking) to common stock, but subordinate to bonds in terms of claim (or rights to their share of the assets of the company).

Preferred stock usually carries no voting rights, but may carry a dividend and may have priority over common stock in the payment of dividends and upon liquidation. Terms of the preferred stock are stated in a “Certificate of Designation”.

Similar to bonds, preferred stocks are rated by the major credit-rating companies. The rating for preferred is generally lower, since preferred dividends do not carry the same guarantees as interest payments from bonds and they are junior to all creditors.

Preferred stock is a special class of shares which may have any combination of features not possessed by common stock. The following features are usually associated with preferred stock:

- Preference in dividends

- Preference in assets, in the event of liquidation

- Convertibility to common stock.

- Callability, at the option of the corporation

- Nonvoting

Capitalization Structure

There are then two interrelated considerations here:

- Management must identify the “optimal mix” of financing – the capital structure that results in maximum firm value, – but must also take other factors into account.

Financing a project through debt results in a liability or obligation that must be serviced, thus entailing cash flow implications independent of the project’s degree of success. Equity financing is less risky with respect to cash flow commitments, but results in a dilution of share ownership, control and earnings. The cost of equity is also typically higher than the cost of debt – which is, additionally, a deductible expense – and so equity financing may result in an increased hurdle rate which may offset any reduction in cash flow risk.

- Management must attempt to match the long-term financing mix to the assets being financed as closely as possible, in terms of both timing and cash flows. Managing any potential asset liability mismatch or duration gap entails matching the assets and liabilities respectively according to maturity pattern or duration; managing this relationship in the short-term is a major function of working capital management, as discussed below.

Conclusion

Corporate finance aims to obtain finances through the right sources to manage day-to-day and long-term financial activities. It strategizes how a company uses and manages capital to maximize value. Planning appropriate capital budgeting and structures is vital for balancing risk and profitability.