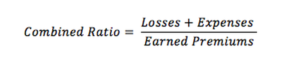

The combined ratio helps the insurance company measure operations and the daily performance. In other words, it measures the operational profitability of the insurance company. It is the sum of expenses and incurred losses divided by earned premium.

Therefore, Combined Ratio= Incurred Losses + Expenses/Earned Premium. The representation is in percentage. The combined ratio is the outflow of money from an insurance company via dividends, losses, and expenses. Losses arise when there is indiscipline in underwriting policies. Insurance companies act as underwriters as they determine the risk of insuring individuals or institutions, and later compensate for the losses occurring in future.

The expense ratio measures the efficiency of the insurer. It tells how optimally the insurer uses the resources to drive the top-line growth. Here, expenses are the general expenses incurred for daily operations.

What does the Combined Ratio indicate?

As mentioned earlier, the combined ratio is represented in percentages. There is an inverse relationship between the combined ratio and profits. Hence, maintain a low combined ratio of expenses and losses to maximize profitability. If the combined ratio is below 100%, it indicates that there are underwriting profits, the premiums collected are more than the claim amount and other related expenses. On the other hand, a combined ratio above 100% depicts underwriting losses, indicating the insurer paying out more claims than receiving premiums.

The combined ratio is the best way to gauge the success of an insurance company because it does not include any investment income. It only shows the profits earned via efficient management. Hence, a combined ratio above 100% does not mean that the insurance company is not profitable as it excludes investment income. The insurance company invests a part of the premium received into various securities like bonds, equities, etc. The investment income ratio includes the investment income as well as the operating profits. Therefore, the combined ratio solely indicates the operational profitability of the insurance company.

Few terms related to insurance

- Premium is a regular amount paid to the insurer for an insurance policy.

- A claim is a formal request to the insurer to compensate the policyholder for losses or policy events.

- Earned premium is the amount that the insurer receives from the policyholder on regular basis- monthly, quarterly, or annually. On the other hand, an unearned premium is an amount that the insurer has not received or earned because the policy is still left to expire. For instance, the total insurance premium while signing the contract was ₹1,20,000. The policy was taken for 12 months and the monthly premium paid is ₹10,000. After the completion of three months, the insurer received ͅ₹30,000 in total from the insured. The remaining ₹90,000 is an unearned premium for the insurer.

- Moreover, the insurance company also creates Loss Reserves which is an estimation of the future claims that the company might need to pay.

- Also, Underwriting Expenses are the expenses incurred to assess the risk like actuarial review, physical inspections, etc. to know whether accept or decline the risk.

- Further, Net Written Premium is the amount of insurance premium an insurance company keeps with itself. It is the total amount of premium received over a certain period plus the reinsurance premium assumed minus the premiums ceded towards reinsurance.

- Lastly, Loss Adjustment Expense is the cost that an insurer incurs to settle and investigate claims. For example, an individual takes car insurance, and an accident damages the car. Now, the insurance company might incur expenses to go to a mechanic and assess the extent of damage to provide the claim.

Examples of Combined Ratio

For instance, an insurance company collects ₹10,000 as a premium and pays ₹8,000 as a claim amount on happening of an unforeseen event to the individual. The company also incurs claim related expenses of ₹1,500. The formula of Combined Ratio= Incurred Losses + Expenses/Earned Premium. Therefore, the combined ratio= 8,000 + 1,500/10,000, which is 95%. Hence, the insurance company is having an underwriting profit.

Another example is an insurance company that incurs underwriting expenses of 10 lakhs and losses and loss adjustment expenses of 15 lakhs. The net written premiums and earned premiums are 30 lakhs and 25 lakhs, respectively. The formula of Combined Ratio= Incurred Losses + Expenses/Earned Premium. Therefore, we add the underwriting expenses and loss adjustment expenses and divide them with the earned premium. Hence, 10 lakhs + 15 lakhs/25 lakhs is 1 or 100%. Hence, the combined ratio is 100%.

For instance, an insurance company collects ₹10,000 as a premium and pays ₹12,000 as a claim amount on happening of an unforeseen event to the individual. The company also incurs claim related expenses of ₹2,000. The formula of Combined Ratio= Incurred Losses + Expenses/Earned Premium. Therefore, the combined ratio= 12,000 + 2,000/10,000, which is 140%. Hence, the insurance company is having an underwriting loss.

Difference between Combined Ratio and Loss Ratio

- Loss and combined ratios help to measure the profitability of an insurance company. Loss Ratio means total losses in comparison to the premiums received or earned. On the other hand, the combined ratio means the total incurred expenses and losses in comparison to the earned premiums.

- Loss Ratio= Total incurred losses/Earned Premiums

- Combined Ratio= Incurred losses + Expenses/Earned Premium

- There is an inverse relationship between loss ratio and profitability. If the loss ratio is more than 100%, the insurance company is unprofitable. For example, the losses amount to three lakhs and the premiums collected amount to two lakhs. Therefore, Loss Ratio is 3,00,000/2,00,000 which is 150%. Since the loss ratio is more than 100%, the insurance company is unprofitable.

- The combined ratio is the money flowing out of the insurance company in form of losses, expenses, and dividends in comparison to the premiums earned. A combined ratio of more than 100% means that the company pays out more claims than the premiums received. But that does not mean that it is not profitable because it does not include investment income. For instance, a company incurs losses of 7 lakhs and 5 lakhs as expenses. It receives 60 lakhs as premiums. Therefore, the combined ratio= 7,00,000 + 5,00,000/60,00,000 which is 20%. Therefore, the company is in good financial health.

To conclude, the combined ratio shows the operational profitability of an insurance company, excluding investment income. It measures the cash outflows of the insurer against the premiums received.